Concentrix: AI Roadkill or Deep Value?

AI displacement narratives have made Customer Experience the most hated sector on Wall Street. Yet, CNXC's growth is accelerating. At just 2.7x EPS, is this the most asymmetric play against AI doom?

TL;DR: Bears said AI would kill the business. It hasn’t. Growth is accelerating. Margins compressed but should recover. At 2.7x adjusted EPS, the opportunity is asymmetric.

When I first wrote about Concentrix roughly two years ago, the stock was already deeply out of favour. The narrative was simple and compelling: AI would automate customer interactions, hollow out call centres, and structurally impair Customer Experience (CX) businesses. The stock was priced as if the business were heading into an irreversible decline.

To me, this was an all-too-familiar story. We have seen versions of it before – with email, with the internet, with offshoring. Each time, the same fear: that technology would eliminate the need for human interaction, and that efficiency gains would translate into revenue losses. Each time, reality proved the bears wrong. Take Teleperformance – Concentrix’s closest peer – which has grown CX revenue every single year since 2003!

Two years later, my position is underwater. I was way too early, which is to say very wrong. With FY2025 behind us, it feels like the right time to revisit assumptions, and ask an honest question: was the thesis wrong?

⠀

I. The Business and the Debate

What does Concentrix do?

Concentrix is one of the world’s largest customer experience (CX) specialists. They design, build, and operate customer-facing functions on behalf of their clients – from creating comprehensive CX strategies, to building the platforms (websites, chatbots, call centres), to optimising processes and leveraging data for continuous improvement.

Ever had to change airline tickets? Complain about a defective product? Make an insurance claim? Report social media content? Chances are that CNXC or one of their peers was on the other side.

The benefit to clients is twofold: improved customer engagement and satisfaction, and cost optimisation. Clients span technology, consumer electronics, travel, e-commerce, media, financial services, healthcare, and beyond. CX outsourcing has historically been a remarkably stable business, with long and sticky contracts, growing in line with GDP.

The Key Debate

The bear case is straightforward: generative AI will automate a large portion of customer interactions, structurally reducing the need for human agents and decimating CX providers’ revenues. The most extreme version of this thesis implies that companies like Concentrix are melting ice cubes – their core product will simply cease to exist.

My counter-thesis has been equally clear: AI is more likely to be a growth driver than a revenue cliff. There are several reasons for this:

AI is likely to lead to a growth in CX outsourcing. It is currently estimated that 66-70% of CX is still done in-house. More of this work can now be outsourced for better outcomes at a lower cost – leading to an expanding TAM for AI-enabled CX specialists.

AI is also driving consolidation that benefits the larger players. CX outsourcing is a highly fragmented market, with the top 8 players barely holding a 30% share. The gap in capabilities is driving customers to consolidate vendors, to the benefit of large players.

AI offers an opportunity to move up the value chain, by designing, implementing and managing full CX offerings (from the tech platform to the human or AI agent). This leads to stickier and larger opportunities. No one is better positioned to do it in a safe and cost-efficient way than legacy CX outsourcers, thanks to their deep domain expertise.

Against those arguments is the view that AI will dramatically reduce the need for human interaction and / or have a deflationary impact on prices. And while there are signs of that in CNXC’s earnings, I would contend that automation has been a decades-long, ongoing process, which hasn’t prevented the CX market from growing.

The CX industry successfully navigated the rise of the internet and “pre-GPT” AI – both turned out to be additional sources of revenue and efficiency gains rather than existential threats. The bear case therefore relies on a “this time is different” type of argument.

What the Valuation Implies

At ~$33 per share, the market values Concentrix at roughly 2.7x FY26 adjusted EPS. That multiple only makes sense if you assume a rapid and sustained erosion in earnings power.

In other words, the bears have completely won in the market’s eyes – even as the business continues to grow.

Interestingly, credit markets appear less pessimistic than equity markets. Concentrix’s 2033 notes are trading at a yield of around 7.4% – higher than earlier this year but very far from distressed.

Equity and debt markets are telling two very different stories.

⠀

II. Reviewing My Calls: Where I Was Right

The central disagreement with the bear case was not that AI would not change the industry – it clearly would, and did. Instead, it was that AI would not destroy it, and potentially even help it grow.

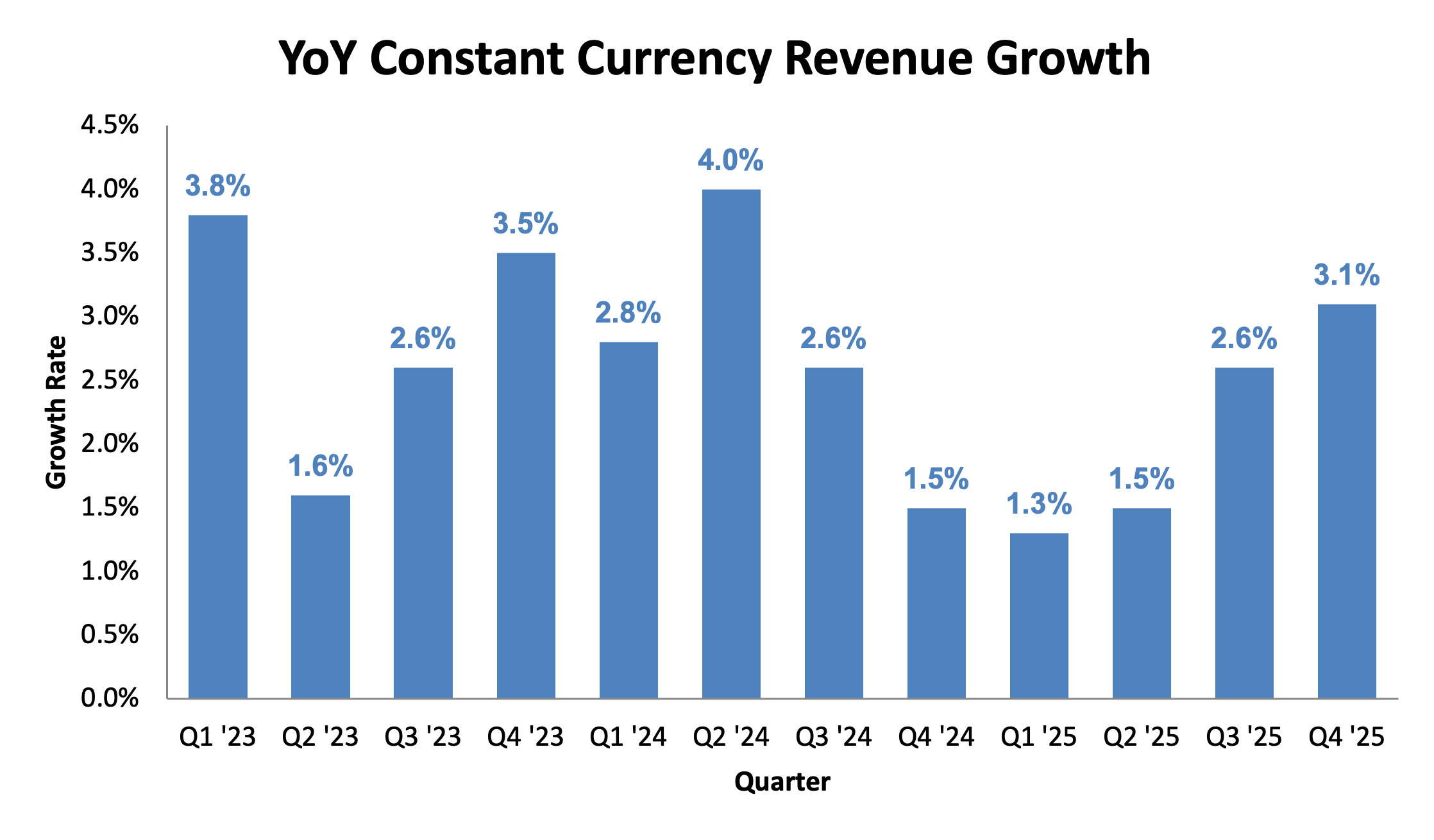

Unlike narratives, facts are stubborn. More than three years after the launch of ChatGPT, Concentrix is still growing. Tellingly, growth has accelerated each quarter since bottoming at 1.3% in Q1 FY25, exiting the latest quarter at 3.1%. This is no small feat in an environment where many expected the business to be in structural decline.

More importantly, the company is winning business of higher quality, and at an increasing rate. From the latest earnings call:

9% increase in new wins year-over-year

6% increase in pipeline annual contract value

14% increase in transformational deal values

23% increase in cross-sell and upsell deals

37% increase in values for new service areas

This is critical. If AI were already displacing CX providers in a meaningful way, we should be seeing it in the pipeline and new business first. We are not.

Instead, what we are seeing is clients asking Concentrix to help them deploy AI safely and efficiently, not replace humans entirely. Automation is being used to remove low-value, low-margin, repetitive work. Human agents are being pushed up the value chain, dealing with complexity, judgment, and exceptions.

This aligns with what I originally believed: AI is a productivity and capability tool for CX companies, not a death sentence.

⠀

III. Where I Was Wrong: The Margin Story

That said, some humility is required.

I underestimated how long the transition phase would last – and how much the cost of building new capabilities and acquiring new customers would weigh on margins.

The expenses of onboarding new, more complex contracts, investing in proprietary AI tools, integrating the Webhelp acquisition, and re-architecting delivery models are very material.

The company invested $95m in new capabilities, capacity, facilities, security, and footprint in FY25 alone. They spent an incremental $25m on go-to-market capabilities and another $25m+ on their iX Suite AI platform.

Similarly, offshoring has accelerated beyond expectations as clients push for cost reductions – 4% of onshore volumes shifted to offshore centres in FY25. This migration incurs duplicate costs for a period of time before the margin benefits materialise.

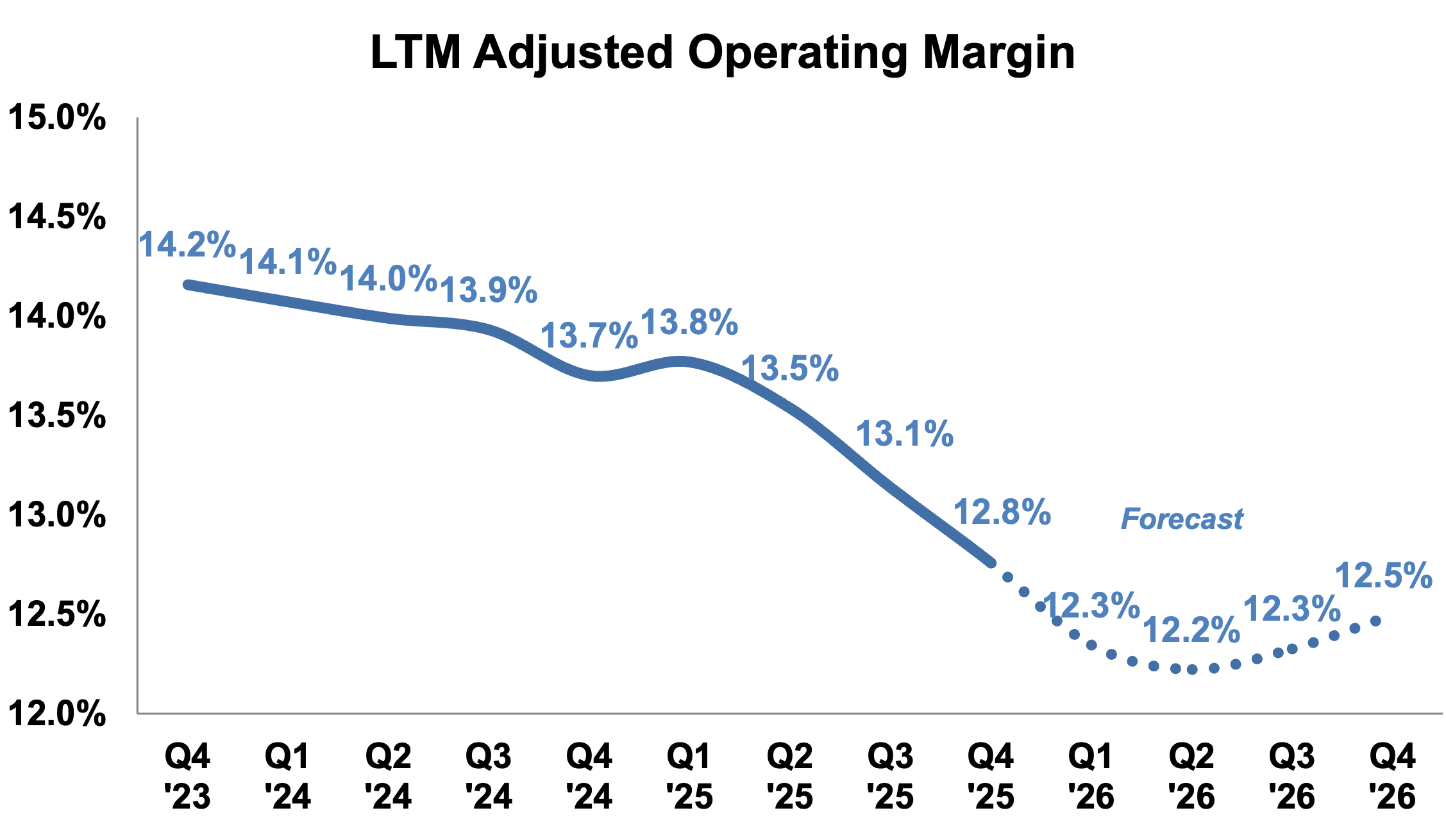

The chart tells the story plainly. LTM adjusted operating margin peaked at 14.2% in Q3 ‘23 and is expected to decline to approximately 12.2% by Q2 ‘26. This is a meaningful compression – roughly 200 basis points of margin lost over ten quarters.

I also underestimated how unwilling the market would be to look through this transition phase. The bear thesis seamlessly pivoted from “revenue destruction” to “margin headwinds.” But isn’t this thesis creep? The original fear was that AI would kill revenues. Revenues are growing. Now the fear is that margins are compressed. Margins are indeed compressed – but largely due to investments that are driving future growth and – likely – profitability.

In hindsight, I was right on the direction of the business, but wrong on the timing and the severity of the margin impact.

⠀

IV. Why CNXC Is Not a Dead Business

Current evidence strongly suggests that Concentrix is not a dying company. It is a business undergoing a transition toward a higher-quality, managed service / AI integrator business model.

The Revenue Quality Transformation

Pure call-centre work – the low-complexity, high-volume interactions that AI can most easily automate – now represents only 5% of the business, down from 7% just a year ago. Management was explicit: they achieved this reduction largely by deploying their own technology to automate work, and by walking away from low-margin business.

Conversely, CX-adjacent services – including data annotation, analytics, financial crimes and compliance, IT services, and digital assets – now represent approximately 20% of revenues and are growing at high single digits. The company is successfully diversifying its revenue base toward higher-growth, higher-value services.

The vast majority of revenues now come from managed services that blend technology, data, and human expertise. And more than 40% of new business wins include Concentrix’s own technology as part of the solution – well ahead of initial expectations. The company is not fighting AI; instead, it is integrating it into its core offering.

Client Stickiness

Average tenure among the top 25 clients is now close to 18 years. 98% of the top 50 clients rely on Concentrix for more than one solution. This is not a business with customers running for the exits – quite the opposite, as integration is deepened by AI solutions.

The AI Software Opportunity

Perhaps most encouraging: CNXC’s iX Suite AI platform has reached $60m in annualised revenue and is now profitable – as committed at the start of the year. From a speculative venture, it has turned into a contributing line of business and commercial differentiator.

In short, the company is moving from experimentation to execution, and is rapidly improving the quality and stickiness of its revenue base.

⠀

V. The Numbers: Summary P&L and Return Opportunity

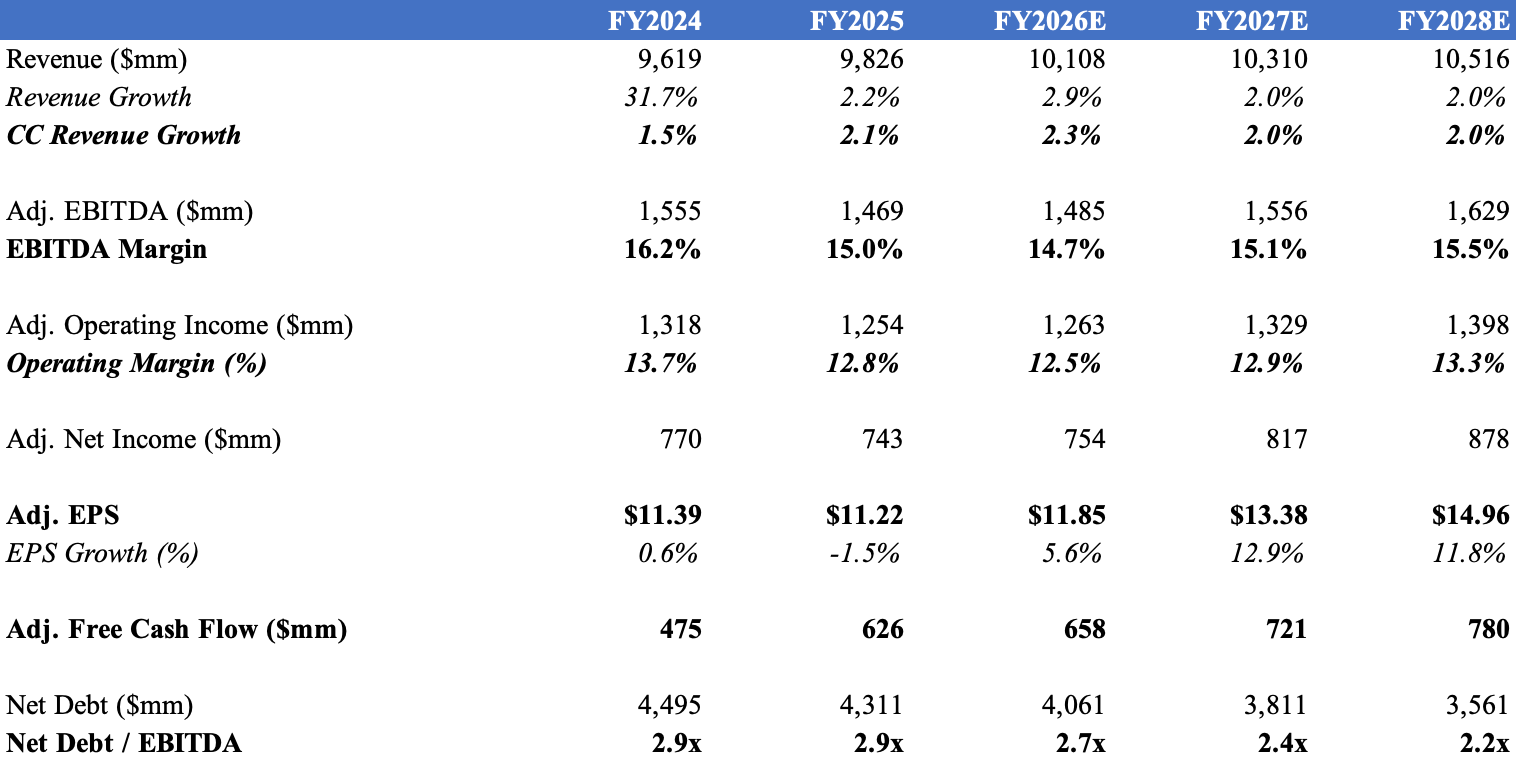

With the qualitative picture in place, let’s look at the numbers. Here is the simplified financial picture:

Source: Company filings and guidance as of January 13, 2026. E = Estimate based on company guidance and model assumptions. CC = Constant Currency.

My assumptions for FY2027: Revenue growth of 2% (constant currency), operating margin expansion of 40bps (as investment phase matures), share buyback rate of 1% per quarter (net of share-based compensation), and debt paydown of $250m annually.

Opportunity

Given the recent past, the current valuation meaningfully discounts management’s guidance. But in my view, they likely learned their lesson and guided margins very conservatively.

Assuming Concentrix meets its guidance, generates increased FCF and accelerates debt repayment, I expect the multiple to progressively re-rate. If in January next year, the company guides to FY27 EPS > $13, a multiple of 5x gives a share price > $65 – roughly 100% upside from current levels.

Is 5x a demanding multiple? Hardly. Business services peers trade at 6–10x, with similar growth rates. Teleperformance has traded at an average of 20x in the 10 years prior to GPT release. Even 5x assumes the market continues to apply a meaningful discount for AI risk – just not quite as extreme as today’s 2.7x.

And if the market refuses to rerate the stock, the 25% FCF yield will ensure appropriate shareholder returns, especially as the company reaches its leverage target in late 2027 or early 2028.

⠀

VI. Risks

What could derail the thesis?

1. AI disintermediation. Many CX AI pilots have failed, slowing adoption. Integrating models, workflows, data governance, and human escalation paths is complex – and this complexity is part of the opportunity for integrators like Concentrix. However, the risk is that CX tooling becomes so turnkey (and trusted) that large enterprises are eventually able to implement and operate it safely and cost-efficiently without external partners.

2. Revenue growth disappoints. If macro weakness, price competition, or aggressive offshoring cause revenue to disappoint, the stock will likely suffer. The company remains a very modest grower (1.5–3% constant currency for FY26), leaving little room for error.

3. Margins don’t recover. Management is guiding to sequential margin improvement in the back half of FY26. Unfortunately, that’s a slippage from last quarter, which itself was a slippage from the previous quarter. If investment costs persist or intensify, or if competitive pressures / AI force pricing concessions, margins could remain compressed or decline further.

4. Debt. The acquisition of Webhelp in 2023 led to a large debt load that will need to be refinanced in 2028-2029. At $4.3bn, net debt represents a multiple of close to 3.0x EBITDA and 6.7x levered FCF. I expect this to impact near-term shareholder returns as progress needs to be made ahead of refinancing. On the positive side, debt repayment should quickly reduce interest expenses, leading to faster FCF growth.

Key mitigant: Valuation. The primary mitigant is valuation. At under 3x adjusted EPS, the market is already pricing in significant impairment. For the stock to decline meaningfully from here, the outcome would need to be worse than the near-death scenario already embedded in the price.

If I am wrong and the business declines 10–15% over several years, the stock probably goes sideways. If I am right and the business stabilises and grows modestly, the stock likely doubles. The risk/reward is asymmetric.

While sentiment could push the stock lower than fundamentals dictate, the 25% FCF yield provides downside protection if one is willing to be patient.

⠀

VII. Catalysts

Catalyst #1: Execution

The most important catalyst is simply meeting or exceeding the plan. If Concentrix can continue to grow revenues modestly (1.5–2%+ constant currency), deliver on its margin guidance (sequential improvement in H2), and generate free cash flow as expected ($630–650m in FY2026), then the market will eventually be forced to reassess its assumptions.

Specifically, margin recovery is key. Management guided to sequential quarterly increases in operating income in the back half of FY26 as they remove duplicate costs, complete transformational deal implementations, and drive automation. If the company can demonstrate even 50bps of margin recovery in the coming quarters, it would signal that the investment phase is maturing and the transition is succeeding. This would cause free cash flow and EPS to jump, likely triggering a re-rating.

Catalyst #2: Capital Allocation

CNXC generates substantial free cash flow – $626m in FY25, a 32% increase and over $150m more than the prior year. Management has committed to share repurchases at a similar pace to FY25 (when they bought back $169m of stock at an average of ~$47/share), continued debt reduction toward target leverage, and maintaining the dividend.

Buying back stock at under 3x adjusted EPS is highly accretive. While the debt load limits share repurchases in the near term (to a still respectable 6–7% of total shares per annum), I expect the company to reach its leverage target by early 2028, in time for refinancing. After which, the 25% FCF yield can be entirely dedicated to accretive buybacks or M&A.

Catalyst #3: Market Recognition

Sometimes, the market simply takes time to recognise value. Each quarter that CNXC grows – rather than contracts – chips away at the bear thesis. As CEO Chris Caldwell put it: “Despite three years of speculation, we are proving that AI is a tailwind for our business.” Time is on our side.

Markets increasingly move on momentum, and a sustained reversal from here would likely feed on itself and turn the current doom loop into a virtuous circle.

⠀

VIII. Conclusion

My conclusion today remains strangely similar to two years ago.

Concentrix does not need heroic growth to justify a materially higher valuation. It simply needs to: (1) continue growing modestly, (2) execute on its margin guidance, and (3) continue to reduce debt and buy back shares.

The last two years have not been clean: margin guidance was missed repeatedly, and debt reduction has been slower than I would have liked as transition costs crept up. That’s fair criticism.

But the core thesis – that AI would not destroy the business – has held. Revenue is growing. The company is winning new business. AI is being integrated, not resisted. Low-complexity work has been reduced to just 5% of the business. The quality of revenue has never been higher.

I still believe this is a business that is more likely to emerge as an AI winner than an AI casualty. The market is taking much longer than I expected to recognise it – which means my timing was poor.

But at under 3x earnings, with the business still growing and generating significant free cash flow, I remain comfortable holding the position. The next year only needs to show progress on margins for the stock to work very well.

I hope you enjoyed the read, and welcome any feedback.

Hugo

──────────────────────────────────────

Disclaimer: I am long Concentrix. This is my investment notebook, not financial advice. Always do your own research.

This is a large position of mine at $80. It is insane that we are seeing $25. Holding on at this point.

Hi Hugo thanks for the insightful read, one question: why do you prefer Concentrix rather than Teleperformance?